The Finance Act 2022 was enacted on 15 December 2022. Amongst other changes to pensions, the Act confirmed that the Benefit in Kind for an employee, which was previously triggered by an employer contribution to a PRSA, has been removed. This has come into effect on 1 January 2023.

Impact for Employees

For ordinary employees saving for retirement in a Personal Retirement Savings Account (PRSA) this is a positive change. They will now be given the same tax treatment as occupational pension scheme members in relation to any employer contributions to their pension scheme. Previously where an employer paid into the PRSA, that employer contribution used up part of the employee’s own scope within their age-related limits to pension their income. This is no longer the case. Employee contributions are still subject to the age-related contribution limits and the Earnings Cap (currently €115,000).

Impact for Business Owners

The changes have led to much discussion as to what it means for employer contributions to a PRSA, particularly in terms of how they are controlled. Currently our interpretation is that the legislation does not place any upper limit on an employer contribution to a PRSA as would exist in occupational pension schemes under the Revenue guidance for Ordinary Annual and Special Contributions.

This in effect means someone could be drawing a salary of €50,000 from the business and make a pension contribution of €1,000,000. This is an extreme example and is certainly not the basis for the change in legislation but it is true and currently allowed under the legislation.

An employer can only make a contribution to a PRSA for an Employee. To be specific, that is someone who is registered as an employee of that entity and receiving a salary under Schedule E with PAYE Taxation applied at source. However thereafter the level of salary paid, service to date and level of pension benefits already accrued are not factored into the ability of that employer to contribute to the PRSA. There is no maximum funding calculation to determine the ability of the employer to contribute as would exist within occupational pension schemes.

Some business owners may see this as an opportunity to fund the pension of a spouse/partner who has been employed in the business but, for whatever reason, never previously attended to their pension funding.

The only limits now seem to relate to the Lifetime Pension Fund Limit (Standard Fund Threshold, currently €2M) – and the Employers capacity to fund a significant contribution and the profits/corresponding tax that the Employer is paying. We have no specific guidance in the Pensions Manual as to how an employer would seek tax relief on such a contribution (as we do for occupational pension schemes in Chapters 4 & 5 of the Revenue Pensions Manual), however, the current interpretation by the industry of the legislation is that it appears these contributions will be allowed as an expense in the year in which they are paid (with no upper limit).

Impact on Advice for Business Owners

Many company directors will already be funding their retirement using an occupational pension scheme often referred to as an executive pension arrangement. For many, the funding rules within those schemes will allow more than enough scope for the contributions they wish to make for their retirement.

However, some company directors will see the new PRSA changes as advantageous. This is likely to be the case for those on low salaries with little or no scope to fund under an occupational pension scheme and also those on larger salaries who have large profits which they want to extract now and obtain tax relief immediately. Another aspect of the PRSA that some directors may find attractive is the more simplistic approach to a death benefits claim for an active member as PRSA funds can be paid in full to the estate of the deceased member in the event of death whereas occupational pension schemes place restrictions on the maximum allowable lump sum payable with residual funds being used to provide a pension via an Annuity or purchase an Approved Retirement Fund (ARF) for a spouse or dependents. As with occupational pension schemes, employers funding an employee’s retirement using a PRSA should always ensure they are compliant with Revenue’s Salary Sacrifice rules.

20% Directors of Investment Companies

The Revenue has been quite clear that a 20% director of a company that is treated for tax purposes as an investment company, could not be accepted into membership of an occupational scheme in relation to that employment. That continues to be the case for executive pension arrangements however no such restriction currently exists in respect of PRSAs. As a result, the current interpretation within the industry is that where a 20% director of an investment company is registered as an employee of that company and receiving a salary under Schedule E then the employer could make an employer contribution to a PRSA for the benefit of that director

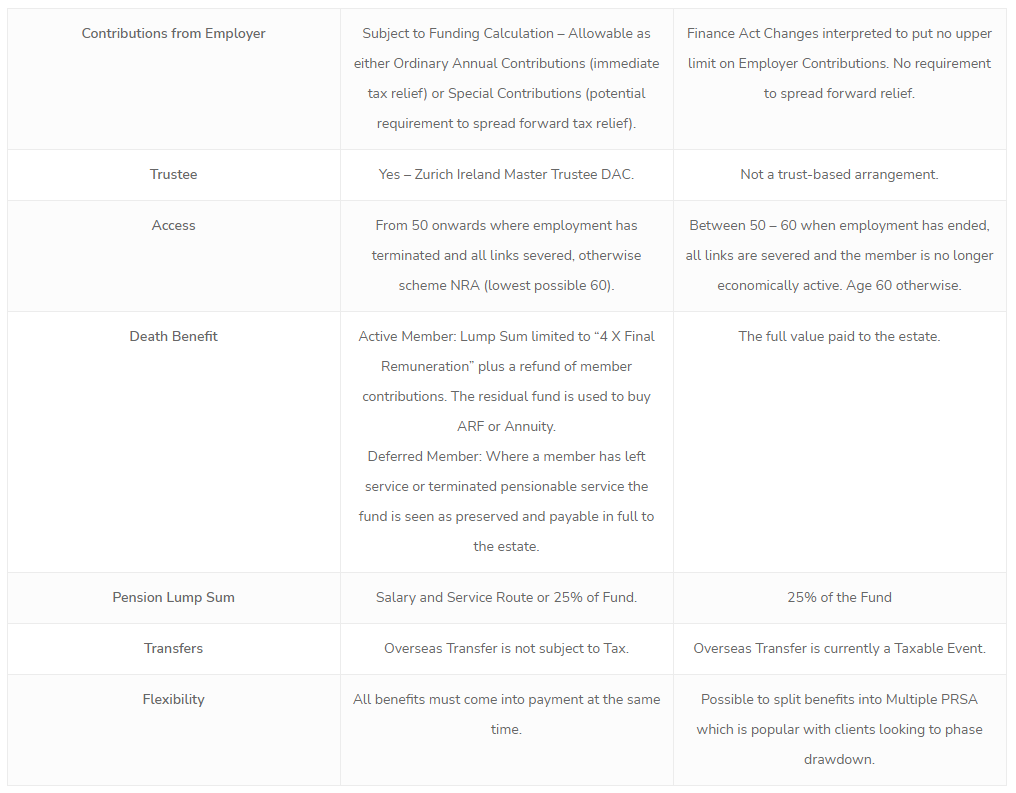

The table below shows the difference between the 2 options available to business owners for funding their pension. The ‘Retail Master Trust’ is essentially the new version of the old Executive Pension.

Retail Master Trust PRSA

Got a Question?

Let us help

-

Icon Accounting, Columba House, Airside,

Swords, Co. Dublin, Ireland, K67 R2Y9