Largely driven by the government’s Climate Action Plan 2021 to lower emissions, 2023 saw the introduction of new measures in calculating Benefit In Kind (BIK) on company vehicles.

Benefit in Kind is a tax charge on an Employee or Director when they have use of a company vehicle.

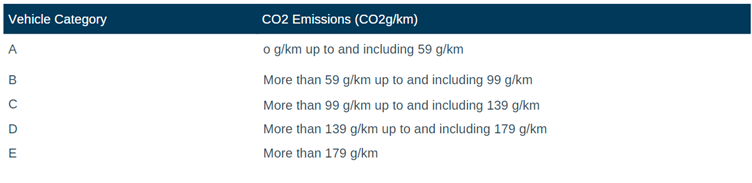

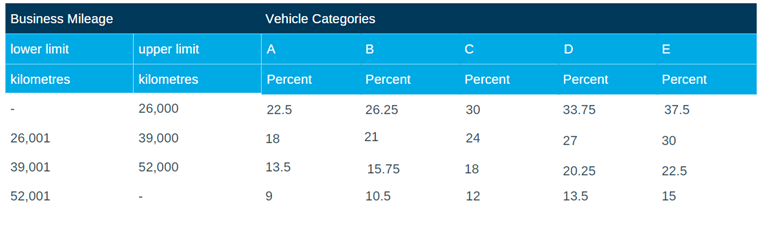

For company cars, there is now a key focus on the CO2 emissions these vehicles release, and it is calculated by taking the Original Market Value of the vehicle, multiplying it by a % depending on the business mileage undertaken and the vehicle’s CO2 emissions.

Please find a table below for calculations.

For company vans, a different calculation will apply, with BIK increasing from 5% to 8%.

Finally, as part of Budget 2022, the Department of Finance have announced the phasing out of the 0% Benefit-in-kind for Electric Vehicles over the next 4 years. From January 2023, we will see the threshold reduced yearly, and once the threshold is reached, 22.5% BIK will apply.

Thresholds to apply to Electric Vehicles Per Year

2023 - Threshold changes to €35,000

2024 - Threshold changes to €20,000

2025 - Threshold changes to €10,000

2026 – No threshold on Bik of 22.5% on Original Market Value

Why is the CO2 based BIK system being changed?

With the move to the CO2 based BIK system since 1 January 2023, an estimated 150,000 drivers with use of a company vehicle have seen a significant jump in their tax liabilities since the updates came into effect, with many concerned that changes to BIK calculations have resulted in a opposite effect to what the policies initially planned.

Thankfully, in early March, we seen the Government recognise the rising tax implications the changes have created, and the pressure this has created for many families living through the cost-of-living crisis. In recognition of this, the Finance Bill 2023 will see a temporary relief introduced on the Original Market Value (OMV) of some vehicles, upon which the tax is calculated.

“The Government remains committed to the environmental rationale behind the current emissions-based vehicle Benefit-in-Kind regime which has been in operation since 1 January 2023,” said Minister for Finance, Michael McGrath. “In the current inflationary context, however, we recognise the difficulty experienced by some people facing BIK increases under the new regime. To that end, I am announcing that the Government is providing temporary changes to BIK for the current year which will help to mitigate some of the increases associated with the new emissions-based calculation.”

What temporary measures are now in place?

The Original Market Value (OMV) of cars will be reduced by €10,000 which will consequently reduce the BIK charge.

The upper limit in the highest mileage band will also temporarily reduce by 4,000km.

When does the temporary relief take effect?

The changes are to be applied retrospectively from January 1st, when the reforms were first introduced and will remain in place until the end of the year. As these changes are effective from 1 January 2023, this may mean making a once-off adjustment to BIK for company vehicles in upcoming payroll submissions to capture the excess BIK applied. Alternative, tax returns submissions can capture this excess too.

Who is the temporary relief applicable to?

The relief will apply to the OMV of cars in the categories of A-D, it won't, however, apply to the E category.

How does it now work when calculating BIK?

An employee has the use of a car provided by his or her employer on 1 January 2023.

The car produces 115g/km in CO₂ emissions, putting the vehicle in Category C. The actual business kilometres in the year are expected to be 50,000 kilometres. The OMV of the car is €50,000. With the new temporary measure applied, the OMV will reduce to €40,000.

BIK Calculation: Cash Equivalent (OMV) €40,000 x 18% = €7,200.

Where can I find more information?

You can find more information at - https://www.gov.ie/en/press-release/fb192-minister-mcgrath-announces-temporary-change-to-benefit-in-kind-regime-for-vehicles-in-finance-bill-2023-cost-of-living-measures/

Have any further questions?

If you are a client of Icon Accounting, you can reach out to your Account Manager at any stage for assistance by emailing info@iconaccounting.ie or by calling 01-8077106.

Got a Question?

Let us help

-

Icon Accounting, Columba House, Airside,

Swords, Co. Dublin, Ireland, K67 R2Y9